Sigh. The moment has come to call a spade a spade. The Chinese property bust is smashing iron ore. Thermal and coking coal are still falling and/or catching up to past falls in contract prices:

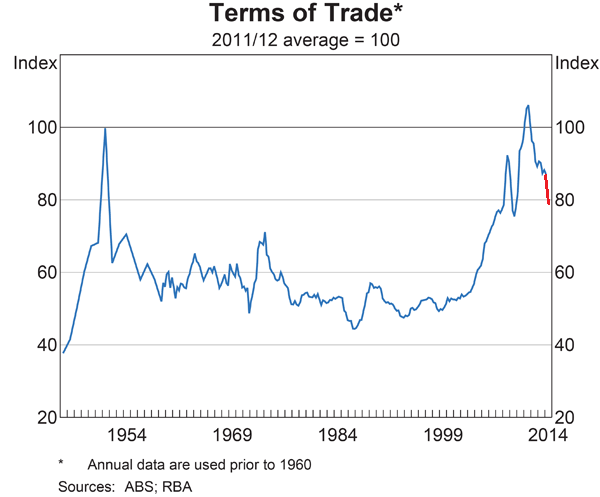

Gold and oil/LNG are also down sharply in the past few months. In short, Australia’s terms of trade (ToT) are getting smashed to the extent that it’s rapidly assuming the proportions of an external shock, especially since the Australian dollar has totally detached itself from the economy.

I can only estimate the ToT falls in train but can say with confidence that they are much bigger than forecast by Treasury or the RBA. Here is my best guess of what’s coming down the pipe in the next three quarters:

Mercifully, thanks to a decent developed economy recovery, we’re being spared the equity debt shocks that usually transpire at the same time and income shock is not as big as the GFC hit (yet!) but it’s big enough to cause all sorts of economic fallout including:

- hitting nominal growth hard and triggering more major Budget revenue misses by the time of MYEFO and then again in Q1 and Q2 next year

- accelerating the mining bust and pushing up unemployment

- deepening falls in per capita income and wage weakness

All of these are being made worse by the Australian dollar, which is now trading exclusively upon the state of European and US monetary policy. It should be at 80 cents and sinking.

In my May post, Five Reasons to Fear Australian Recession, I explored a worrying convergence of factors that could tip the economy into a major funk. They were:

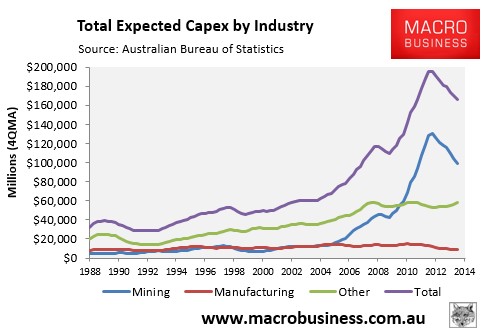

- the mining investment cliff

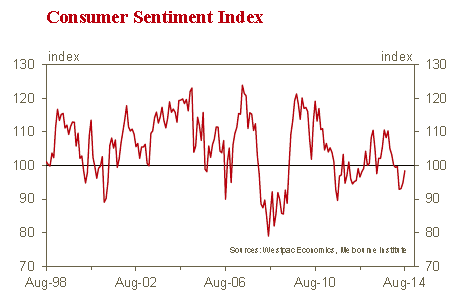

- weak consumer confidence

- the Sydney and Melbourne investor mortgage blowoffs

- a terms of trade shock

- an Australian dollar that refuses to fall

Let’s update the five. The first is getting worse not better and will move even more quickly as commodity prices sink:

The second has recovered moderately but remains gloomy:

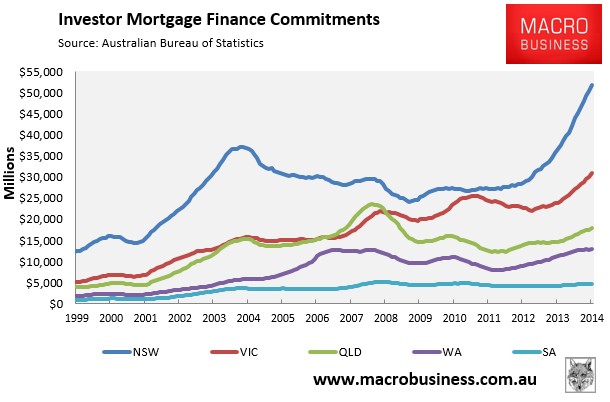

The third has gotten much worse and is vulnerable to a sudden reversal of sentiment. Fundamentals are falling away with rental and immigration growth slowing fast:

The fourth is underway and the fifth is not responding as it should.

Q2 growth was already a virtual recession with the only real hope of dragging it up the arithmetic calculation of inventories. Q3 is not going to be much better. And the terms of trade and Budget fallout will roll out progressively over the next three quarters. I concluded in May that:

The possible convergence of these five negative waves in the third quarter would swamp the economy. Consumer confidence leads house prices and if it remains weak, and the external shock arrives, then Sydney and Melbourne housing could roll over just as mining-related job losses rise in WA and QLD as the Gorgon and QCLNG projects begin the construction wind down.

That’s an income shock, labour market stall and negative wealth effect plus public austerity. Real activity in the national economy will resemble last year’s second half domestic demand recession even if measures like net exports hold up, only this time housing will be coming off not rising.

I’m bringing forward my next rate cut to October, with a possible follow up soon afterwards. And that brings me to the real problem. If these events do converge, why would a lousy 50bps make much difference?

I’ve since lifted the October call on RBA delusion but retain an easing bias. The next move is definitely down, as soon as housing slows. 2015 is going to be rough.